Quick Answer: Ireland’s top-performing pension funds in 2026 are concentrated in global equity and managed growth categories. Providers including Irish Life, Zurich, New Ireland, and Aviva all offer high-growth funds with 5-year annualised returns in the 8–12% range. However, the ‘best’ pension plan for you depends on your age, risk appetite, retirement timeline, and tax position, not just fund performance tables. This guide explains what to look for, and how Joe Coyle Financial Consultants in Donegal can help you choose wisely.

If you have searched for ‘best pension plans Ireland‘ or ‘top performing pension funds Ireland’, you have likely been overwhelmed by provider brochures and comparison sites that rank funds by last year’s returns alone. That is the wrong way to pick a pension, and one that consistently costs Irish savers thousands of euros over a working lifetime.

At Joe Coyle Financial Consultants, based in Donegal and serving clients nationwide, we have spent over 30 years matching individuals and business owners to the pension investment funds Ireland that genuinely fit their financial goals. Joe Coyle Financial Consultants Ltd is regulated by the Central Bank of Ireland and is part of the Money Maximising Advisors group. For expert pension advice you can also visit Money Sense Financial Services, both regulated by the Central Bank of Ireland.

1. Why Choosing the Right Pension Matters More Than Chasing Performance

Irish pension savers often make the mistake of optimising for the wrong metric. A fund that returned 15% last year may carry much higher volatility risk than your retirement timeline allows. Conversely, a fund that appears ‘safe’ in a low-interest environment may fail to grow your savings fast enough to maintain purchasing power into your 80s and 90s.

The key variables that determine your best pension plan in Ireland are:

Your age and time to retirement: A 32-year-old in Donegal has 30+ years to compound; equity-heavy funds are appropriate. A 58-year-old switching into drawdown needs a different strategy entirely.

Your risk tolerance: Some clients are comfortable watching fund values dip 20% in a market correction; others are not. Your advisor must understand your psychology, not just your balance sheet.

Your tax position: Pension contributions receive income tax relief at your marginal rate 40% for higher-rate taxpayers. A €1,000 pension contribution costs a higher-rate taxpayer just €600 after relief. This makes maximising contributions the most powerful tax planning tool available to most Irish earners.

Your existing pension entitlements: Many Donegal clients have previous employer pensions, public sector entitlements, or overseas pension transfers. These need to be consolidated and planned around, not ignored.

► Book a Free Pension Review with Joe Coyle Financial Consultants

2. The Major Irish Pension Providers Compared

Ireland’s pension market is dominated by a small number of licensed Irish pension providers, all of whom offer a range of funds across risk profiles. Joe Coyle Financial Consultants works with all of the following providers and can give you impartial, unbiased guidance on which best suits your situation:

Irish Life

Ireland’s largest life and pensions provider, with a broad range of managed, multi-asset and specialist funds. Their MAP (Managed Annuity Portfolio) and Indexed Lifestyle funds are popular with investors approaching retirement. Performance: 5-year annualised returns on their higher-equity funds have ranged between 8.5% and 11.2% (Source: Irish Life, 2025 fund fact sheets). Strong digital platform with good online access for policyholders.

Zurich Life

Known for strong global equity and sustainable investment options. The Zurich Prisma range offers risk-graded options from Prisma 2 (very low) to Prisma 6 (very high). Suitable for clients who want a structured, clear risk-level framework. Zurich’s 5-year performance on higher-risk funds has averaged 9–12% annualised return, one of the stronger performers in the Irish market.

New Ireland (Bank of Ireland Life)

New Ireland offers a solid range of with-profits and unit-linked funds. Their Everest range has been popular with clients seeking moderate growth with some downside protection. Good option for clients who prefer a more conservative approach without sacrificing all growth potential.

Aviva

Aviva’s Irish operation offers strong international fund exposure, including a popular Indexed World Equity Fund that tracks global markets at a low cost. Aviva’s passive investment options are worth considering for cost-conscious clients, as annual management charges on indexed funds are typically lower than actively managed equivalents.

Standard Life

Now operating through Phoenix Group in Ireland, Standard Life offers several MyFolio options that provide a blended fund-of-funds approach. Their risk-rated MyFolio range suits investors who want a ‘set and forget’ approach managed by a team of investment professionals.

► Compare Pension Providers — Contact Us Today

3. Understanding Pension Tax Relief in Ireland 2026

The single most important pension fact for every Irish earner is this: pension contributions receive income tax relief at your marginal rate. In 2026, that means:

Standard rate taxpayers (20%): A €1,000 pension contribution costs €800 after tax relief.

Higher rate taxpayers (40%): A €1,000 pension contribution costs just €600 after tax relief.

PRSI and USC savings: Employer pension contributions also save the employer PRSI (11.15% in 2026), making employer contributions one of the most tax-efficient ways to reward employees.

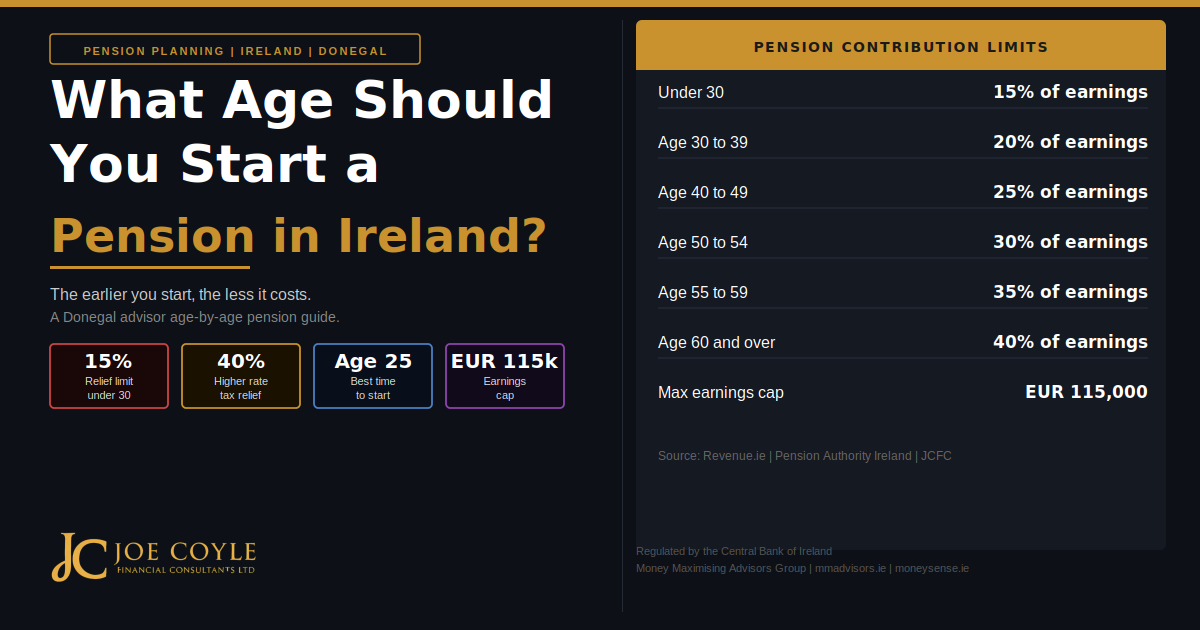

Age-related contribution limits also apply. The maximum percentage of net relevant earnings you can contribute and receive tax relief on is:

Under 30: 15% of net relevant earnings

Age 30–39: 20%

Age 40–49: 25%

Age 50–54: 30%

Age 55–59: 35%

Age 60 and over: 40%

The earnings cap for relief purposes is €115,000 in 2026. The Standard Fund Threshold, the maximum pension fund value you can build up before additional tax applies, is €2 million. Careful pension planning is essential for clients who may approach this threshold.

4. Choosing Between a Defined Contribution and Defined Benefit Pension

Most private sector pension plans in Ireland today are Defined Contribution (DC): your pension pot grows based on contributions made and investment returns earned. Defined Benefit (DB) schemes, common in the public sector — promise a fixed retirement income based on salary and years of service.

For Donegal business owners and private sector employees, DC pensions are the norm. The key decisions are:

Fund selection: Which investment fund(s) to allocate contributions to

Contribution level: Maximising tax-relievable contributions each year

Lifestyle strategy: Gradually de-risking the portfolio as you approach retirement

At retirement: Choosing between an Annuity, an Approved Retirement Fund (ARF), or a combination. Joe Coyle Financial Consultants helps clients navigate every one of these decisions. For retirement income planning also see retirement planning advice Ireland resources at mmadvisors.ie and moneysense.ie.

5. Approved Retirement Funds (ARFs): The Flexible Retirement Option

Since 1999, Irish pension savers have been able to invest their pension fund or a significant portion of it into an Approved Retirement Fund (ARF) at retirement, rather than being forced to buy an annuity. ARFs allow:

Investment flexibility: Your pot stays invested across funds of your choice

Drawdown control: You choose how much income to take each year (subject to a minimum 4% imputed distribution annually from age 61)

Death benefits: The ARF passes to your estate on death (subject to income tax in the hands of beneficiaries)

ARFs are particularly attractive for business owners and higher earners who do not need to lock in a fixed income immediately at age 65. However, they carry investment risk, your fund value can fall as well as rise. Careful fund selection and regular reviews are essential.

► Discuss Your ARF Options Book a Consultation

6. Previous Employer Pensions and Pension Consolidation

One of the most common issues we see at Joe Coyle Financial Consultants is clients who have accumulated multiple small pension pots from previous employers and have lost track of them entirely. Joe Coyle Financial Consultants specialises in previous pension advice and can help you locate, value, and consolidate your existing pension entitlements.

Your options when leaving a pension scheme typically include:

Leave it where it is: Your deferred benefit remains in the employer scheme until retirement

Transfer to a Personal Retirement Bond (PRB): You take control of the investment and can move it to a provider and fund of your choice

Transfer to your new employer’s scheme: Where the new scheme rules permit

7. Overseas Pension Advice: Returning to Ireland from the UK or Further Afield

Many clients working with Joe Coyle Financial Consultants have spent years working in the UK, the US, Australia, or elsewhere and have overseas pension entitlements they are unsure what to do with. The rules around overseas pension transfers to Ireland are complex. Joe Coyle Financial Consultants will assess your specific situation and provide a clear, written recommendation. Learn more about our overseas pension advice service.

► Get Overseas Pension Advice from Our Donegal Experts

8. A Note on Corporate and Directors’ Pensions

For Donegal business owners and company directors, the pension is one of the most powerful tools available, not just for retirement planning, but for tax efficiency right now. A company can make pension contributions on behalf of a director as a deductible business expense, removing the contribution from the company’s taxable profits and simultaneously building the director’s retirement fund.

The interaction between your salary, dividends, corporation tax, and pension contributions is complex. Joe Coyle Financial Consultants works closely with clients and their accountants to structure the most tax-efficient overall package.

Frequently Asked Questions: Pension Plans Ireland

What is the best pension plan in Ireland in 2026?

There is no single ‘best’ plan. The right pension depends on your age, income, risk profile, and retirement goals. Higher-equity funds from Zurich, Irish Life, or Aviva have delivered strong long-term returns, but they suit investors with at least 10 years to retirement. Get personalised advice from a financial advisor in Donegal like Joe Coyle Financial Consultants.

Which pension fund has performed best in Ireland?

Based on 5-year annualised returns to the end of 2025, global equity and multi-asset growth funds from Zurich Life and Irish Life have been among the top performing pension funds Ireland, with returns in the 9–12% range. Past performance is not a guide to future returns.

How do I choose the right pension fund in Ireland?

Start with your time to retirement. If you have 20+ years, you can afford more equity exposure. Work backwards from the retirement income you want, factor in the State Pension (€289 per week in 2026), and calculate the fund size you need. A QFA can run this calculation for you and stress-test it against various return scenarios.

What is the safest pension fund in Ireland?

‘Safe’ in pension terms usually means low volatility cash or bond-heavy funds. These preserve capital but typically deliver lower long-term returns. For long investment horizons, ‘safe’ choices can actually be risky because they may not keep pace with inflation. Discuss your specific risk comfort level with an advisor.

Which pension provider offers the best returns in Ireland?

Returns vary by fund and period. Zurich’s global equity funds and Irish Life’s higher-growth managed funds have performed strongly over the 5-10 year period to 2025. An independent financial advisor can compare the best pension funds Ireland without bias. Past performance does not predict future results.

Can I have more than one pension in Ireland?

Yes. Many people have a combination of a current employer pension, Personal Retirement Savings Accounts (PRSAs), deferred benefits from previous employers, and an ARF from a previous pension drawdown. An advisor can help you manage multiple arrangements cohesively.

► Book Your Free Consultation Book Now

Important Information

This article is for general information purposes only and does not constitute financial advice. Fund performance data referenced is drawn from publicly available provider fact sheets and is correct as at July 2026. Past performance is not a reliable indicator of future results. Joe Coyle Financial Consultants Ltd is regulated by the Central Bank of Ireland (C54725) and is part of the Money Maximising Advisors group (C154250). Always seek personalised advice from a Qualified Financial Advisor before making pension decisions.

Written by: Joe Coyle Financial Consultants Ltd | jcfc.ie | info@jcfc.ie | +353 091 342596

Part of Money Maximising Advisors Group | mmadvisors.ie | moneysense.ie