Quick Answer: To retire comfortably in Ireland in 2026, most financial planners estimate you need a private pension fund of €400,000–€750,000 (depending on your lifestyle expectations), supplemented by the State Pension of €289.30 per week (if you qualify). The State Pension alone equates to approximately €15,000 per year, far below what most people consider comfortable. This guide from Joe Coyle Financial Consultants in Donegal explains exactly how to calculate your retirement number, what the State Pension covers, and how to build a fund that genuinely lasts.

Retirement planning in Ireland is simultaneously one of the most important financial decisions you will ever make and one of the most neglected. A combination of complexity, inertia, and a mistaken faith in the adequacy of the State Pension means that far too many Irish people including many Donegal families who have worked hard all their lives reach retirement planning Ireland with far less financial security than they deserve.

Joe Coyle Financial Consultants, based in Donegal and serving clients nationwide from our head office, has helped thousands of clients navigate the retirement planning journey. We are regulated by the Central Bank of Ireland and part of the Money Maximising Advisors group. Complementary guides and advice are also available from Money Sense Financial Services at moneysense.ie.

This article gives you the real numbers, the correct questions to ask, and a practical framework for retirement planning in Ireland in 2026.

1. What is the State Pension in Ireland in 2026?

The Contributory State Pension in Ireland in 2026 is €289.30 per week approximately €15,044 per year, payable from age 66. To qualify for the full rate, you generally need 520 paid PRSI contributions (10 years of full-time employment), with your contributions assessed on a yearly average basis.

The Non-Contributory State Pension is a means-tested payment for those who do not qualify for the Contributory Pension; the maximum rate is slightly lower. Many self-employed workers, business owners, and people with gaps in their PRSI record receive a reduced Contributory Pension or may not qualify at all.

The critical point: even a full Contributory State Pension of €289.30 per week is unlikely to support the lifestyle most people want in retirement. Annual spending for a single person living modestly in Ireland is typically estimated at €20,000–€25,000 per year; for a couple with a car, heating, and occasional holidays, €35,000–€45,000 per year is more realistic. The State Pension covers less than half of this for a single person.

2. How Much Do You Need to Retire in Ireland? The Real Numbers

There is no universal answer, but the following framework which Joe Coyle Financial Consultants uses with clients gives a useful starting point:

Step 1: Estimate Your Retirement Income Need

Most financial planners use 60–75% of pre-retirement income as a target. If you earn €60,000 today, your target retirement income is €36,000–€45,000 per year. This accounts for the fact that mortgage payments are typically finished, children have left home, and commuting and work costs disappear.

Step 2: Subtract the State Pension

Deduct the State Pension (€289.30 per week = €15,044 per year in 2026). The balance is the income your private pension must provide.

Example: Target income €40,000. State Pension €15,000. Private pension must provide €25,000 per year.

Step 3: Calculate the Fund Size You Need

Assuming you draw down 4–5% of your fund per year (a widely used planning assumption), divide your annual private pension income requirement by 0.04 or 0.05. This is how much do you need to retire in Ireland:

€25,000 ÷ 0.04: = €625,000 fund required

€25,000 ÷ 0.05: = €500,000 fund required

This is a simplified illustration. The actual fund required depends on your investment strategy in retirement, whether you use an ARF or annuity, your health, the size of your tax-free lump sum, and market conditions. A proper retirement plan, which Joe Coyle Financial Consultants will prepare for you, runs a cash-flow model across multiple scenarios.

Step 4: Factor in Inflation

At 2.5% annual inflation, your purchasing power halves in roughly 28 years. A 65-year-old retiring today could live to 93 or beyond. Long-term investment returns must outpace inflation, which means your retirement fund cannot simply sit in cash.

► Get Your Personalised Retirement Number — Book Now

3. How Much Should I Have Saved by Age 50 in Ireland?

A widely used rule of thumb, though it needs to be personalised, is that by age 50, you should have approximately 5–6 times your annual salary saved as retirement savings Ireland. So if you earn €60,000 at age 50, you should ideally have €300,000–€360,000 in pension savings.

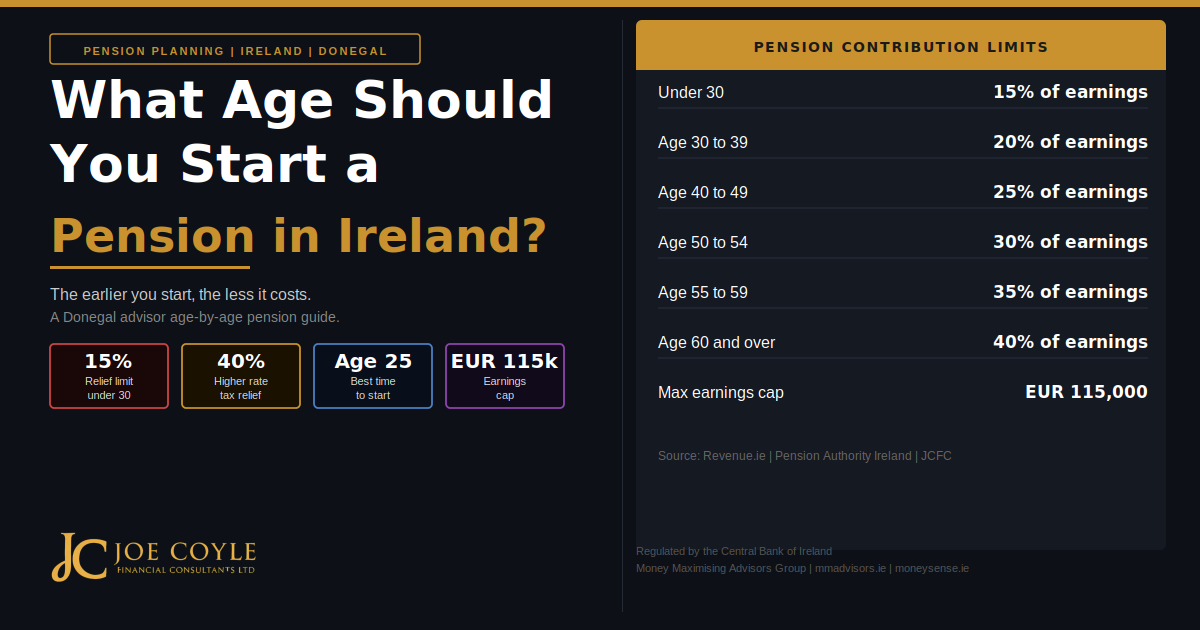

If you are behind this benchmark, do not panic, but do act. The age-related contribution limits increase significantly from age 50 onwards (30% of earnings at 50–54, rising to 40% from age 60), allowing for significant ‘catch-up’ contributions. At the higher income tax rate, these are genuinely powerful.

For clients approaching 50 with a pension shortfall, Joe Coyle Financial Consultants typically recommends a full pension audit assessing all existing pension entitlements, modelling the shortfall, and designing a contribution strategy to close it within the remaining working years.

4. How Much Pension Do You Need to Retire at 65 in Ireland?

Retiring at 65 before the State Pension age of 66 means bridging at least one year without State Pension income. More importantly, it means your private pension fund must last potentially 30+ years.

For a couple both retiring at 65 in Donegal or elsewhere in Ireland, seeking a combined income of €50,000 per year (including eventual State Pensions), a combined pension fund of €600,000–€800,000 is a realistic planning target. Single individuals targeting €35,000 per year should aim for €400,000–€550,000.

These figures vary significantly depending on:

Annuity vs ARF: Annuities provide a guaranteed income for life but typically deliver lower starting incomes than ARF drawdown. ARFs offer flexibility but carry investment risk

Health: Poor health can affect annuity rates (positively enhanced annuities for health conditions) and the expected duration of drawdown

Property: If the family home is owned outright, living costs in retirement are significantly lower

Other income: Rental income, part-time work, or defined benefit entitlements all reduce the requirement from the private pension

5. Can I Retire Comfortably on the Irish State Pension Alone?

For the vast majority of Irish people, the answer is no. The full Contributory State Pension of €289.30 per week (€15,044 per year) does not cover the cost of a comfortable retirement in Ireland, particularly given rising energy costs, healthcare expenses in later life, and the cost of maintaining a household.

The Society of Actuaries in Ireland has estimated that a ‘modest but comfortable’ retirement for a single Irish person requires approximately €25,000 per year; for a couple, approximately €38,000 per year. The State Pension covers approximately 60% of the single person’s requirement and under 40% of the couple’s requirement.

The gap is real and it is growing. Private pension savings are not optional, they are essential for everyone whose standard of living in retirement matters to them.

► Discuss Your Retirement Income Gap — Contact Us

6. What is the Average Pension Pot in Ireland?

According to the Pensions Authority and recent Central Statistics Office data, the average pension pot in Ireland at retirement is significantly below what is needed for a comfortable retirement. Many Irish workers, particularly those in the private sector with gaps in employment or who started their pension late, retire with between €100,000 and €250,000 in private pension savings.

This shortfall is one of the primary reasons the Irish government introduced auto-enrolment a mandatory workplace pension planning Ireland scheme beginning in 2025 which will gradually enrol all eligible employees who are not already in a workplace pension. Auto-enrolment is a positive development, but contributions under auto-enrolment start low (1.5% employer, 1.5% employee, 0.5% government in Years 1–3) and will not on their own produce sufficient retirement funds for most workers.

The responsibility for adequate retirement planning remains individual and the window for meaningful pension building is most open in your 30s, 40s and early 50s. If you are reading this in that age bracket in Donegal or anywhere in Ireland, the best time to act is now.

7. Approved Retirement Funds: Keeping Your Pension Flexible in Retirement

At retirement, most private sector pension holders in Ireland have the option of investing their pension fund or a portion of it into an Approved Retirement Fund (ARF). An ARF allows:

Continued investment growth: Your fund stays invested in the market, continuing to grow (and to carry investment risk)

Flexible drawdown: You choose how much to take as income each year, subject to a minimum imputed distribution of 4% per year from age 61 (6% from age 70 on funds over €2 million)

Inheritance: The ARF passes to your estate on death, with the value taxed as income in the hands of your spouse or child beneficiaries

For clients who need an ARF, or who want to understand the choice between an ARF and an annuity at retirement, Joe Coyle Financial Consultants provides detailed, impartial advice. Annuities provide guaranteed lifetime income but are typically irreversible; the right choice depends on your health, risk tolerance, and income needs.

8. Retirement Planning for Donegal Business Owners and Self-Employed Individuals

If you are self-employed, a company director, or a sole trader in Donegal, your retirement planning situation is distinct from employees. You do not have a default employer pension scheme, the responsibility is entirely yours. But you also have access to some of the most powerful pension structures available:

Financial planning for retirement options available to self-employed individuals and directors include:

Self-Employed PRSA: Personal Retirement Savings Accounts are available to self-employed individuals, with contributions receiving income tax relief at your marginal rate

Executive Pension Plan: For company directors, an executive pension allows the company to make contributions on the director’s behalf, deductible against corporate profits

Self-Administered Pension: For clients with larger funds, a self-administered structure allows investment in property and other non-standard assets within the pension wrapper

Joe Coyle Financial Consultants has deep experience working with Donegal business owners, farmers, and self-employed professionals to build appropriate retirement strategies. For additional resources, see mmadvisors.ie/pensions-advice/ and moneysense.ie/pensions-advice/.

► Book a Free Retirement Review — Book Now

Frequently Asked Questions: Retirement Planning Ireland

How much money do you need to retire comfortably in Ireland?

A realistic target for comfortable retirement planning advice Ireland in 2026 is a private pension fund of €500,000–€750,000, depending on lifestyle expectations, property ownership, and whether you will receive a full State Pension. This is above the average Irish pension pot and requires deliberate, early planning.

What is a good retirement income in Ireland?

A ‘good’ retirement income in Ireland is generally estimated at €35,000–€50,000 per year for a couple, or €25,000–€35,000 for a single person. These figures allow for home maintenance, healthcare, a car, occasional travel, and everyday living costs without significant financial stress.

How much should I have saved by age 50 in Ireland?

A rough benchmark is 5–6 times your annual salary. At €60,000 salary, this suggests €300,000–€360,000 saved in your pension by age 50. If you are behind this benchmark, the higher age-related contribution limits from age 50 onwards give you meaningful ‘catch-up’ capacity but you should start immediately.

How much pension do I need to retire at 65?

To retire at 65 in Ireland on a combined household income of €40,000–€50,000 per year (before State Pension age of 66), a private pension fund of €600,000–€900,000 is a reasonable planning target for a couple. Individual circumstances vary significantly and a personalised projection is always more accurate than a rule of thumb.

Can I retire comfortably on the Irish State Pension?

For most people, no. The full Contributory State Pension is €289.30 per week (€15,044 per year) in 2026. A comfortable single-person retirement requires approximately €25,000 per year; a couple requires approximately €38,000 per year. Private pension savings are essential to bridge this gap.

What is the average pension pot in Ireland?

Available data suggests many private sector retirees in Ireland have pension savings of €100,000–€250,000 at retirement well below the €400,000–€750,000 typically needed for a comfortable retirement. This shortfall is the primary driver of financial stress in retirement and underlines the importance of early, consistent pension saving.

► Start Your Retirement Plan Today — Book a Free Consultation

Important Information

This article is for general information purposes only and does not constitute financial advice. Pension figures, State Pension rates, and tax reliefs referenced are correct as at July 2026. Figures may change in future Budgets. Joe Coyle Financial Consultants Ltd is regulated by the Central Bank of Ireland (C54725), part of the Money Maximising Advisors group (C154250). Past performance of pension funds is not a reliable indicator of future results. Always seek personalised advice from a Qualified Financial Advisor.

Written by: Joe Coyle Financial Consultants Ltd | jcfc.ie | info@jcfc.ie | +353 091 342596

Part of Money Maximising Advisors Group | mmadvisors.ie | moneysense.ie