How do I manage my money better in Ireland in 2026? The most effective money management approach for Irish adults in 2026 follows a 7-step priority order: (1) map your cash flow and net worth; (2) build a 3–6 month emergency fund; (3) clear high-interest debt; (4) maximise pension contributions for up to 40% tax relief; (5) put income protection in place; (6) invest surplus savings; and (7) plan your estate to minimise inheritance tax. Each step builds on the last.

Joe Coyle Financial Consultants, a Donegal-based, CBI-regulated financial broker and member of the Money Maximising Advisors group, has helped thousands of individuals and business owners across Ireland implement this exact framework. Further financial planning resources are available at Money Sense Financial Services.

Most Irish adults manage money reactively: spend first, save what is left. This approach consistently produces poor outcomes , chronic underinvestment in pensions, insufficient protection, unnecessary tax bills, and financial anxiety that compounds over decades. The solution is a clear, prioritised framework. Here it is.

Step 1: Know Your Numbers , Cash Flow and Net Worth

You cannot manage what you do not measure. Before any financial strategy is built, you need two numbers: your monthly cash flow surplus (income minus all spending) and your net worth (total assets minus total liabilities).

Monthly Cash Flow

List every source of after-tax income. Then list every outgoing , fixed (mortgage, insurance, utilities) and variable (food, transport, entertainment). The gap between income and outgoings is your monthly surplus , the raw material of all wealth building. If it is negative, that is the problem to solve before anything else.

Net Worth Snapshot

Add up all assets: current account, savings, pension value, property equity, investments. Subtract all liabilities: mortgage outstanding, car finance, credit card balances, personal loans. The result is your current net worth. Tracking this number annually shows whether your financial position is improving or declining over time.

💡 Most people significantly underestimate their spending and overestimate their savings rate. People who track their spending consistently save 15–20% more than those who do not.

► Build Your Personal Financial Plan , Book a Free Consultation with Joe Coyle

Step 2: Emergency Fund , Your Financial Safety Net

Before you invest a single euro, before you pay extra off your mortgage, and before you maximise your pension, you need a liquid emergency fund covering 3–6 months of essential living expenses.

Why 3–6 months?: This covers job loss, unexpected home or car repairs, reduced income from illness, or any other financial shock without forcing you into debt

Where to keep it: A high-interest instant-access savings account , accessible immediately, earning a return above inflation, separate from your current account

Single vs dual income: Single-income households and self-employed individuals should target 6 months; dual-income households can manage with 3

Rebuild rule: If the emergency fund is ever drawn on, rebuilding it takes priority over all other financial goals until it is restored

Step 3: Eliminate High-Interest Debt

Not all debt is equal. A mortgage at 3.5% is fundamentally different from credit card debt at 23% APR. High-interest consumer debt is the most reliably negative financial decision most people make , because the guaranteed ‘return’ from eliminating 23% APR debt exceeds anything available in the market.

The Avalanche Method , Mathematically Optimal

List all debts by interest rate, highest to lowest. Make minimum payments on all, then direct every available euro to the highest-rate debt first. When cleared, roll the payment to the next. Minimises total interest paid over the repayment period.

The Snowball Method , Psychologically Effective

List debts by balance, smallest to largest. Clear the smallest balance first regardless of interest rate. Each cleared debt generates momentum and motivation. Research consistently shows this method produces better real-world results for people who struggle with long-term consistency.

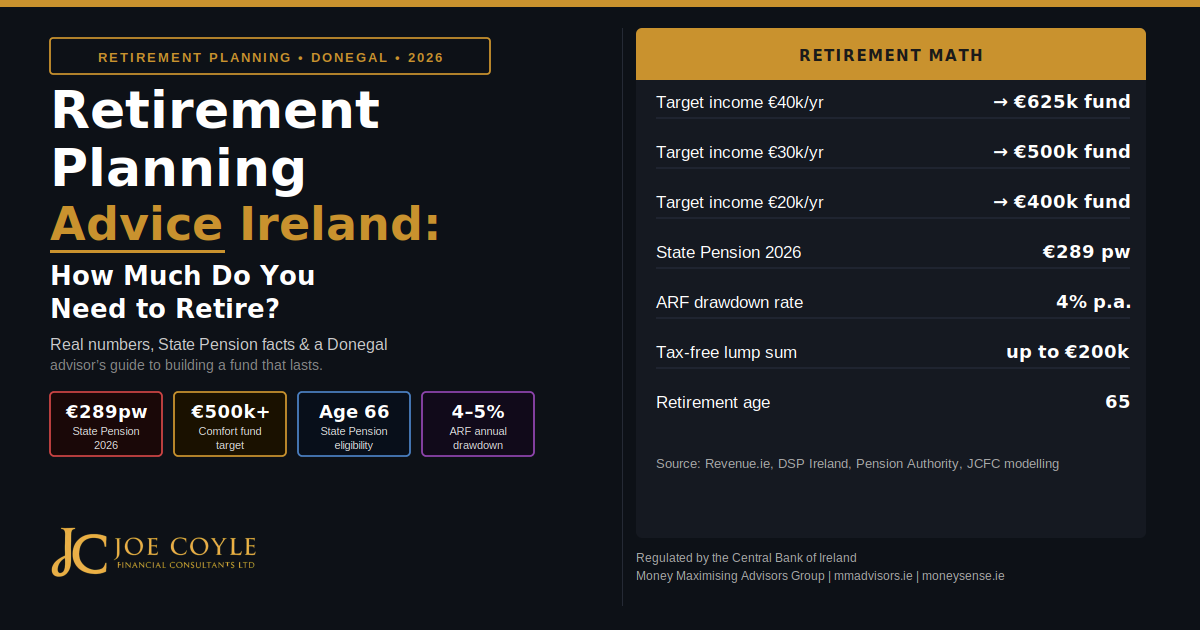

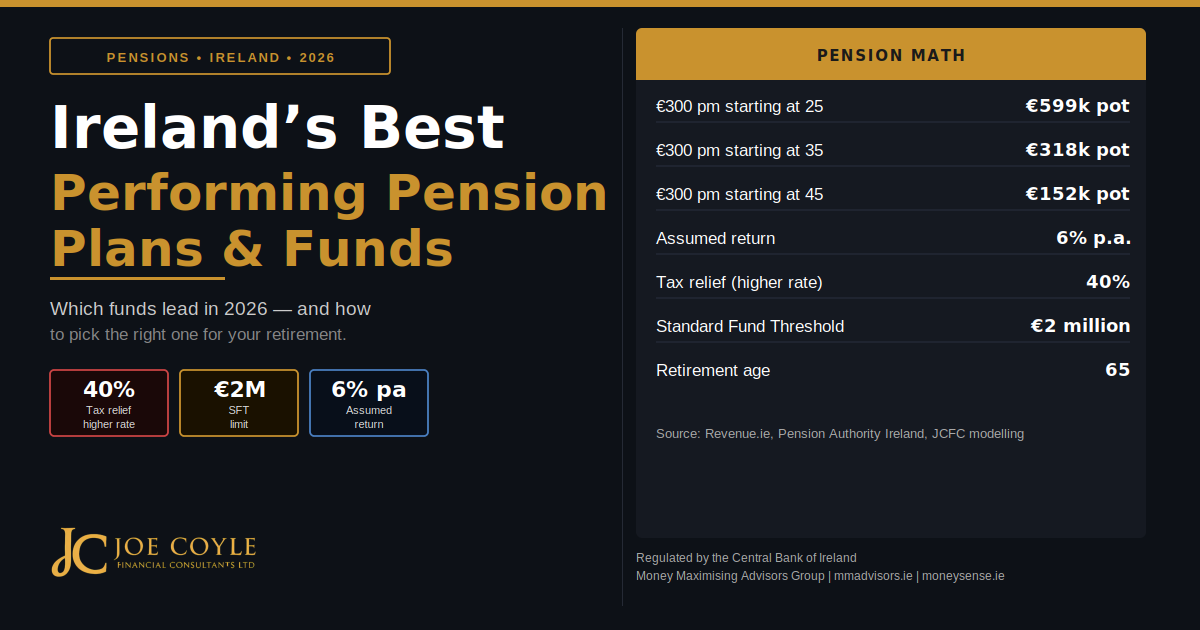

Step 4: Maximise Your Pension , Ireland’s Most Powerful Tax Tool

For most Irish earners, maximising pension contributions delivers the highest guaranteed ‘return’ of any financial decision , not because of investment growth, but because of the income tax relief applied immediately on contribution.

The Maths: Why Pension Beats Almost Everything

A higher-rate taxpayer contributes €1,000 to their pension at an effective net cost of €600 after 40% tax relief. That is a 66.7% guaranteed return before a single cent of investment growth occurs. The fund then grows free of income tax, CGT, and DIRT. At retirement, up to €200,000 can be taken as a tax-free lump sum.

Age-Related Contribution Limits

Under 30: 15% of net relevant earnings

Age 30–39: 20%

Age 40–49: 25%

Age 50–54: 30%

Age 55–59: 35%

Age 60 and over: 40%

The earnings cap is €115,000. Many clients in their 40s and 50s are significantly under-contributing relative to their limit , leaving substantial tax relief unclaimed every year.

💡 If you are a higher-rate taxpayer contributing less than your age-related limit allows, you are effectively overpaying income tax. Joe Coyle Financial Consultants calculates your exact contribution headroom and the tax saving available at your first meeting.

► Maximise Your Pension Tax Relief , View Pensions Advice

Step 5: Protect Your Income and Your Family

No wealth-building strategy survives a serious health event without protection advice Ireland in place. Income protection, life insurance, and serious illness cover are not expenses , they are the infrastructure that prevents one setback from destroying everything you have built.

Income protection: Up to 75% of salary if illness or injury prevents work. Tax-deductible premiums at marginal rate. Essential for self-employed and business owners

Life insurance: Dual life term cover to protect your family’s mortgage, income and lifestyle in the event of death

Serious illness cover: Tax-free lump sum on diagnosis of major conditions , cancer, heart attack, stroke and 60+ others

Business protection: Keyman, co-director and Relevant Life Plans to protect your company and business partners

Step 6: Invest Surplus Savings to Build Long-Term Wealth

Once the first five steps are in place , and only then , does it make sense to invest surplus savings. With a pension maximised and protection in place, additional wealth can be built through:

Approved Retirement Fund (ARF): Continue building wealth inside the tax-efficient pension wrapper post-retirement

Unit-linked investment funds: Diversified global funds via life company wrappers , subject to 41% Exit Tax on gains in Ireland

Direct property investment: Strong long-term returns and rental income, but requires significant capital and hands-on management

State Savings (An Post): Secure, government-backed, tax-free returns up to certain limits , suitable for cautious investors

Direct equities: Higher potential returns for long-term investors comfortable with short-term volatility

Step 7: Estate Planning , Preserve Your Wealth for the Next Generation

The final step is ensuring that the wealth you build passes to the next generation as efficiently as possible. Ireland’s Capital Acquisitions Tax (CAT) at 33% applies to inheritances above the Group A threshold of €400,000. Proactive inheritance tax advice Ireland , through the Small Gift Exemption, Section 72 Policies, and Agricultural or Business Relief , can eliminate or dramatically reduce the CAT bill on your estate.

For Donegal families with property, a farm, or a business, estate planning is as important as any other financial decision. Joe Coyle Financial Consultants works with clients and their solicitors to structure plans that protect family assets across generations.

Frequently Asked Questions: Money Management Advice Ireland

How do I start managing my money better in Ireland?

Start by mapping your monthly cash flow and calculating your net worth. Then follow the 7-step priority order: emergency fund → clear high-interest debt → maximise pension → protection → invest → estate planning. Joe Coyle Financial Consultants builds a personalised plan across all seven areas at your first consultation.

How much should I save each month in Ireland?

A common benchmark is 20% of take-home pay across pension, emergency savings and investments. However, the correct rate depends on your age, existing pension savings, debt position and retirement goals. A 50-year-old with limited pension savings needs to save far more aggressively than a 28-year-old starting early.

Is it better to overpay my mortgage or invest in Ireland?

For most Irish borrowers in 2026 with fixed rates of 3–4%, maximising pension contributions , which carry a guaranteed 40% tax relief , mathematically outperforms mortgage overpayment. However, overpaying provides psychological security and reduces the mortgage term. Joe Coyle Financial Consultants models both options with real numbers for your exact situation.

What is the 50/30/20 budgeting rule and does it work in Ireland?

The 50/30/20 rule allocates 50% of take-home pay to needs, 30% to wants, and 20% to savings and debt. In Ireland’s higher-cost urban markets, 50% for needs is often insufficient. In Donegal and regional areas the rule works more naturally. Joe Coyle Financial Consultants adapts the framework to your specific cost of living and financial goals.

How can I build wealth on an average income in Ireland?

The most powerful tools for average Irish earners are: (1) maximise pension contributions for tax-free compounding; (2) avoid high-interest debt at all costs; (3) put income protection in place so one health event cannot undo years of progress; (4) start investing early , time in the market consistently outperforms timing the market; and (5) get professional advice to avoid the costliest financial mistakes.

What financial planning services are available in Donegal?

Joe Coyle Financial Consultants, based in Mountcharles, Co. Donegal, offers a full range of services: pensions, retirement planning, protection, mortgage comparison, money management, inheritance tax planning, redundancy advice and corporate financial wellness. All advisors are QFA-qualified and the firm is regulated by the Central Bank of Ireland. Nationwide service from our Donegal head office.

Important Information

This article is for general information purposes only and does not constitute financial advice. Tax rate, pension contribution limit, and financial figure figures referenced are correct as at July 2026 and may change. Joe Coyle Financial Consultants Ltd is regulated by the Central Bank of Ireland (C54725), part of the Money Maximising Advisors group (C154250). Always seek personalised advice from a Qualified Financial Advisor before making financial decisions.

Joe Coyle Financial Consultants Ltd | jcfc.ie | info@jcfc.ie | +353 091 342596

Part of Money Maximising Advisors Group | mmadvisors.ie | moneysense.ie